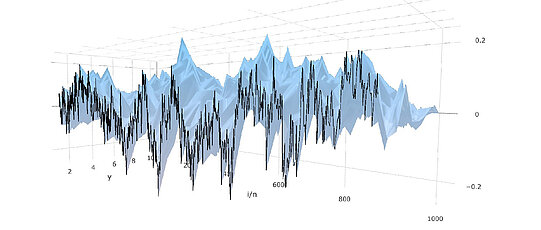

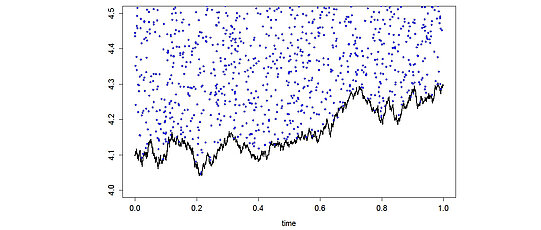

We work on applications of statistics for processes in financial econometrics. We are especially interested in intra-day, high-frequency financial data. For many liquid financial instruments huge numbers of observations are nowadays available ("big data"). In a limit order book, often several price recordings per second are available. Modelling and analysis of such high-frequency financial data becomes more and more important as much volume, currently almost 70%, is attributed to high-frequency trading. No arbitrage considerations motivate to use semi-martingales as stochastic processes to model logarithmic price evolutions. One characteristic of these semi-martingales is the volatility which reflects intrinsic risk due to price oscillations. In the multi-dimensional case, a volatility matrix includes as well the portfolio correlation structure. Additionally, jump components of semi-martingales model large, sudden price changes as response to news and shocks. Price data recorded at ultra-high frequencies is affected by market microstructure noise, such that we require more complex observation models with noise. The estimation of volatility and techniques to separate noise, jumps and continuous price movements in such models are subject of our research.

The methods have been applied, for instance, to distinguish systemic and idiosyncratic risk factors. In a collaboration with researchers at the European central bank, we used high-frequency prices of different government bonds to analyze and compare instruments of communication and market guidance.

To analyze systemic risk factors in large portfolios, we work on theory for high-dimensional, high-frequency financial data.